Category: Accounting

A UAE trading, contracting, or manufacturing business usually enters Saudi Arabia with confidence. The sales team sees demand. Operations sees scale. Finance assumes VAT will be similar enough to manage with a few tax codes and a revised invoice template.

That assumption causes trouble fast.

VAT in Saudi Arabia isn’t just a tax setting. It affects pricing, invoice structure, registration timing, purchase recovery, branch controls, and how your ERP talks to ZATCA. If your company operates in both the UAE and KSA, the problem gets bigger because your team is already managing different compliance expectations across markets. A finance manager in Abu Dhabi may be comfortable with UAE VAT workflows, but that doesn’t mean the same setup will survive scrutiny in Saudi operations. For businesses trying to grow without creating audit exposure, an integrated system matters from day one. If you already deal with regional tax changes, this broader view on new tax obligations in the UAE is a useful comparison point.

The practical mistake I see most often is this: companies treat KSA VAT as an accounting issue after the sale happens. That’s too late. By then, the wrong invoice may already be issued, the wrong tax treatment may already be posted, and the compliance risk may already be sitting in your ledger.

A serious business should treat Saudi VAT as an operational process. Sales, procurement, warehouse, projects, finance, and IT all need to work from the same logic. If they don’t, you won’t get clean reporting, and you won’t get reliable compliance.

Chat on WhatsApp +971506228024 Quotation – Demo RequestIntroduction The Modern Business Guide to Saudi Arabian VAT

A company can be profitable on paper and still create VAT risk every week.

That’s common when a UAE-based business opens a Saudi branch, starts supplying customers in Riyadh or Dammam, and keeps using the same workflow it used in the UAE. The sales invoice gets raised. Stock moves. Payments arrive. Then finance realises the tax treatment, invoice format, and reporting expectations in KSA aren’t aligned with what the team is doing on the ground.

Where businesses usually get stuck

The friction doesn’t start with tax theory. It starts with daily operations:

- Sales teams quote incorrectly: They may apply the wrong tax assumption when pricing a customer order.

- Procurement teams post purchases badly: Input VAT recovery becomes messy when documentation and coding aren’t disciplined.

- Branch operations work in isolation: One office may follow one invoice process while another branch follows something else.

- Finance cleans up too late: Manual corrections at month-end don’t fix poor source transactions.

Practical rule: If your VAT treatment depends on spreadsheet corrections after posting, your process is already weak.

Why ERP matters early

Saudi VAT compliance only works properly when your business system controls the transaction before it reaches the ledger. That means customer master setup, item tax mapping, invoice generation, approval rules, and tax reporting all need to be connected.

This is why businesses expanding into KSA should configure their ERP before volume builds. Waiting until filings become difficult is expensive. It creates rework, confuses branches, and increases audit exposure.

KSA VAT Fundamentals Rates Scope and Taxable Supplies

Saudi Arabia introduced VAT on January 1, 2018 at 5%, and the rate increased to 15% on July 1, 2020. A YouGov survey after the increase found 91% of residents were financially affected. By 2026, the standard rate remains 15%, according to Statista’s Saudi VAT revenue overview.

For business owners, the important point is simple. 15% is the default position. If your supply doesn’t clearly fall into a zero-rated or exempt category, treat it as standard-rated until your tax position is verified and correctly configured in your system.

The three categories you must separate properly

A lot of internal confusion comes from mixing up standard-rated, zero-rated, and exempt supplies. They are not interchangeable, and your ERP should not treat them loosely.

| Supply category | What it means in practice | Common business implication |

|---|---|---|

| Standard-rated | VAT applies at the standard rate | You charge VAT on sales and typically recover eligible input VAT on related purchases |

| Zero-rated | VAT applies at 0% | You don’t charge VAT to the customer, but you may still recover eligible input VAT |

| Exempt | No VAT is charged | Input VAT recovery is generally restricted on related costs |

What this means for day-to-day operations

For a trading company, most normal local sales activity falls into the standard-rated category. For an exporter, the treatment may differ if the transaction qualifies as zero-rated. For businesses dealing in financial services or specific exempt activity, the bigger issue is often blocked input recovery rather than output tax itself.

That distinction matters because many finance teams only focus on what goes out to customers. Strong VAT management also depends on how purchases are posted. If your accounts payable team records exempt-related costs under the wrong logic, your input VAT position becomes unreliable.

Zero-rated sales and exempt sales may both show no VAT to the customer. They do not create the same recovery outcome for the business.

The ERP setup should follow commercial reality

Don’t rely on one generic tax code across your item master and service catalogue. That creates avoidable errors. Instead, configure tax handling around the actual structure of the business:

- By item or service type: Goods, services, rentals, projects, and exports often need different handling.

- By transaction nature: Local sale, inter-company movement, export, advance billing, and credit note workflows should not be merged.

- By business unit: A contracting division and a trading division rarely have identical VAT behaviour.

- By document type: Quotations, sales invoices, debit notes, and purchase invoices shouldn’t all follow the same posting assumptions.

Businesses that organise vat in saudi arabia this way make fewer corrections, produce cleaner returns, and handle audits with less chaos.

Chat on WhatsApp +971506228024 Quotation – Demo RequestVAT Registration Thresholds and Procedures

A common failure looks like this. Sales start in Saudi Arabia, operations push invoices out, finance plans to “sort VAT later,” and the business discovers the registration trigger after taxable supplies have already crossed the line. By then, the problem is no longer administrative. It is a control failure.

Saudi VAT registration is mandatory once annual taxable supplies exceed 375,000 SAR. Voluntary registration applies from 187,500 SAR. Non-resident businesses making taxable supplies in the Kingdom often cannot rely on a threshold at all and must assess registration from the start, based on the ZATCA VAT registration guidance.

Act before the threshold is crossed

Do not wait for audited accounts or year-end review. Registration risk should be tracked weekly inside your ERP, by legal entity, with taxable sales visible in real time.

Pay close attention if your business falls into one of these groups:

- New Saudi market entrants: Early project billing, deposits, and first-phase supply contracts can push turnover up faster than management expects.

- Businesses with multiple branches or divisions: Internal reporting may split revenue, but ZATCA assesses the obligation at the entity level.

- Non-resident sellers and digital providers: Cross-border activity needs tax review before the first invoice goes live.

- Fast-growing SMEs: Growth hides compliance gaps. A strong sales quarter can create a registration issue before finance closes the month.

Voluntary registration should be a planned decision

Voluntary registration is not just a tax technicality. It affects purchasing, pricing, invoicing, and customer confidence.

Register early if you are incurring input VAT, selling mainly to VAT-registered business customers, and expect sustained growth. Delay usually creates rework. Finance ends up correcting old invoices, procurement cannot recover VAT cleanly, and operations keep using customer and item masters that were never set up for tax compliance.

Late registration is avoidable. Poor visibility is usually the real cause.

Build the procedure into your ERP, not into a spreadsheet

The ZATCA portal is only the final submission point. The actual registration process starts inside your operating system.

Your internal procedure should include:

- Threshold monitoring by legal entity with dashboards that isolate taxable supplies from exempt and out-of-scope activity.

- A named tax owner responsible for registration status, portal setup, and evidence retention.

- Customer and supplier master data checks so tax treatment is assigned correctly before transaction volume increases.

- Approval rules for new revenue streams such as online sales, contracts, branch activity, and digital services.

- ERP alerts and workflow triggers that flag threshold exposure before the business crosses it.

The practical importance of automation is clear. An ERP such as Hinawi ERP should not just record sales. It should classify transactions correctly, warn management when the threshold is approaching, and prepare the business for compliant invoicing from day one. That is how you prevent late registration, rushed fixes, and avoidable penalties.

The VAT Compliance Cycle Returns Payments and Record-Keeping

Month-end closes. Finance is chasing missing supplier invoices, sales has issued credit notes outside policy, and the VAT return is due. If that sounds familiar, your VAT process is too dependent on cleanup.

Registration gets you into the system. Discipline keeps you compliant. In Saudi Arabia, the filing cycle, payment process, and audit trail have to run on schedule every period, with figures that reconcile back to source transactions.

Output VAT and input VAT must reconcile cleanly

Your return stands on one calculation. Output VAT from taxable sales, less recoverable input VAT from eligible business purchases.

The problem is not the formula. The problem is transaction quality. Advance receipts, partial deliveries, debit and credit notes, landed costs, inter-branch activity, retention billing, and late supplier documents all affect the return. If your sales ledger, purchase ledger, inventory postings, and tax codes do not match, finance ends up adjusting numbers manually. That is a control failure, not a reporting method.

Saudi VAT rules also require the business to follow the correct filing frequency based on turnover, and accounting treatment matters because smaller businesses may qualify for cash basis while larger ones must stay on accrual. If your ERP is not configured around those rules, the return will be technically filed but operationally weak.

KSA VAT Compliance at a Glance 2026

| Compliance Area | Rule / Threshold | Implication for Businesses |

|---|---|---|

| Mandatory registration | 375,000 SAR annual taxable supplies | Monitor turnover continuously and register on time |

| Voluntary registration | 187,500 SAR to 375,000 SAR | Smaller businesses may register to improve input VAT recovery |

| Non-resident digital providers | No threshold | Registration is required from the first relevant B2C sale |

| Late registration penalty | 10,000 SAR | Delays create direct financial exposure |

| Filing frequency | Quarterly below 40M SAR, monthly above 40M SAR | ERP scheduling and closing discipline must match filing frequency |

| Cash basis option | Allowed if supplies are ≤5M SAR | Smaller businesses may reduce upfront VAT pressure on receivables |

| Standard VAT rate | 15% | Most taxable transactions must default to this treatment unless clearly classified otherwise |

Treat VAT as a system cycle. Sales creates the tax point. Purchasing determines recoverability. Inventory affects cost allocations. Finance posts the final entries and submits the return. If any one of those steps is handled outside the ERP, risk increases.

For finance teams, the practical fix starts with ledger control. Tax accounts, suspense accounts, vendor accruals, and adjustment journals should be visible and reviewable before submission. If your team needs tighter posting discipline, this guide to the general ledger structure in accounting is directly relevant.

Chat on WhatsApp +971506228024 Quotation – Demo RequestRecord-keeping is not an admin task

Record-keeping is your audit defence.

Every figure in the VAT return should trace back to an invoice, credit note, payment record, customs document, purchase entry, or approved journal. That includes tax codes, amendment history, user actions, and document timestamps. Branches that store documents in email threads and shared folders create avoidable exposure because evidence gets lost, versions conflict, and finance cannot prove why a VAT treatment was applied.

Good VAT compliance leaves a traceable record. Bad VAT compliance leaves a story.

Hinawi ERP should be configured to do more than store transactions. It should control tax code usage, block incomplete postings, link source documents to ledger entries, and keep return data ready for review by entity, branch, project, or business line. That is how multi-industry GCC businesses reduce filing errors, support ZATCA audits, and stop rebuilding VAT returns in spreadsheets every period.

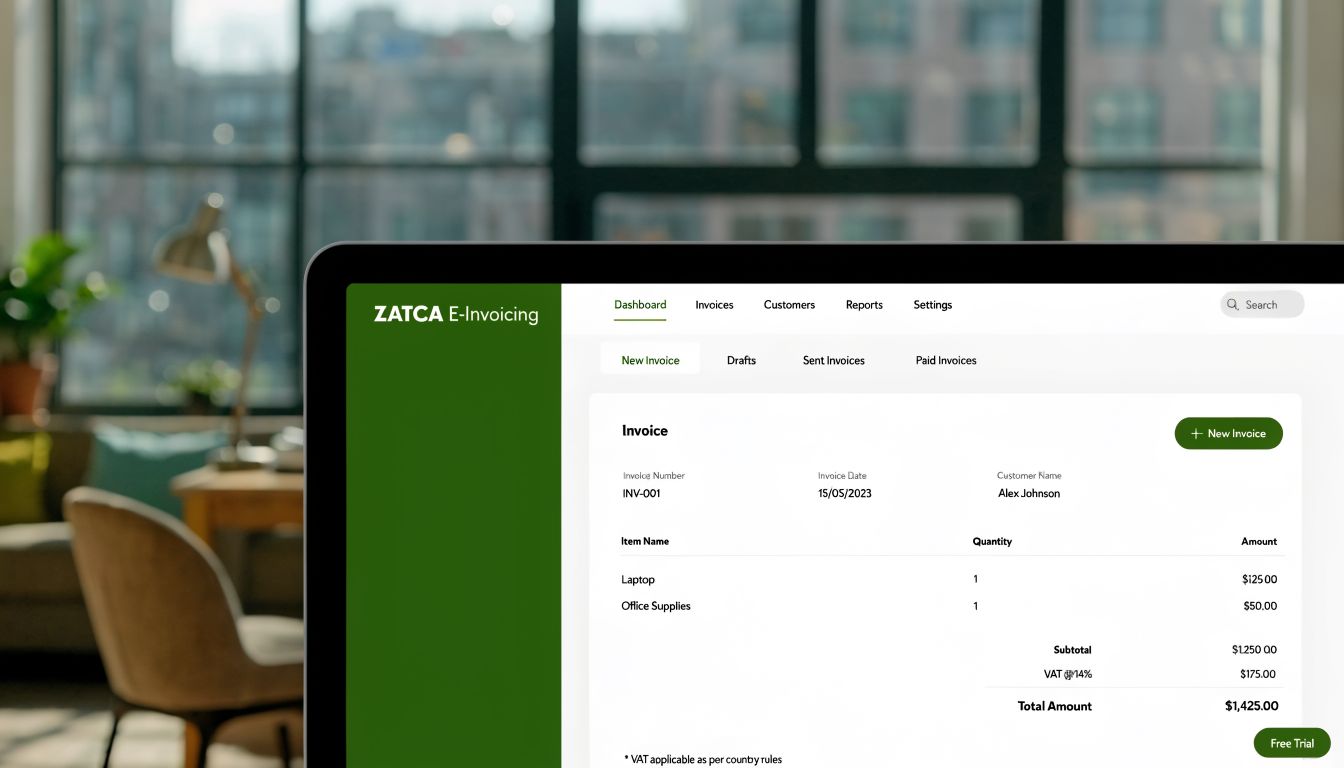

Navigating ZATCA E-Invoicing The Fatoora Mandate

Most VAT problems in Saudi Arabia don’t start in the tax return. They start at invoice level.

ZATCA’s e-invoicing framework forced businesses to move beyond loose invoice templates and disconnected billing tools. Once invoice generation becomes part of tax compliance, your software architecture matters. Basic accounting packages and manually edited invoice formats aren’t enough when the invoice itself has to meet regulatory requirements consistently.

What businesses get wrong about e-invoicing

A lot of managers still think e-invoicing means “send invoices as PDF”. That’s not the operational issue. The core issue is whether your invoicing process follows ZATCA-compliant structure, timing, tax logic, and integration requirements.

The Saudi VAT guidance used earlier notes simplified tax invoices under 1,000 SAR can omit the supplier VAT number, and it highlights the need for reliable AR and AP linkages to ZATCA’s Fatoora portal. That matters because invoice design is no longer only a branding matter. It is now part of your compliance infrastructure.

The process has to be system-driven

A workable setup should handle:

- Correct invoice classification based on customer type and transaction nature

- Tax calculation at source rather than manual override after posting

- Credit and debit note logic tied to the original transaction

- Audit trail retention for edits, cancellations, and resubmissions

- Branch-level consistency so every location follows the same rules

If you’re still trying to bolt e-invoicing onto an old process, you’ll keep generating exceptions.

Why integration beats patchwork

The safest route is to use an ERP that manages invoicing and accounting together. When the invoice is created inside the same system that posts receivables, stock movement, project billing, and tax entries, control improves immediately. One practical example is Hinawi ERP’s KSA e-invoicing and QR code workflow, which shows how invoice compliance can be embedded in daily transaction processing rather than handled as a separate IT patch.

If your tax compliance depends on users remembering extra invoice steps manually, the process won’t hold under scale.

For retailers, contractors, service firms, and manufacturers, the lesson is the same. E-invoicing in Saudi Arabia is not an optional module sitting beside finance. It belongs inside the transaction engine of the business.

Advanced VAT Scenarios Reverse Charge and Cross-Border Rules

Cross-border activity is where many GCC businesses lose control. The transaction looks commercially normal, but the VAT treatment changes because the supplier is abroad, the customer is in another jurisdiction, or the place of supply isn’t what the team assumed.

The practical challenge becomes sharper for groups operating across the GCC. As noted by EZ Integrated’s discussion of GCC VAT differences, businesses often have to manage Saudi Arabia’s 15% VAT environment alongside the UAE’s 5% framework. That’s exactly why a single regional business can’t rely on one generic tax workflow.

Reverse charge needs discipline

A common risk scenario is imported services. A Saudi entity buys software, consulting, design, or technical support from a foreign supplier. The foreign invoice may arrive without Saudi VAT. That does not mean the transaction is outside Saudi VAT consequences.

In these cases, the buying entity often needs to account for the VAT treatment internally through reverse charge logic. If finance doesn’t identify the transaction properly, the business may understate tax obligations or misstate recoverable input.

The control point should sit inside procurement and accounts payable, not only in tax review after month-end.

Cross-border ERP logic must be separated by jurisdiction

A GCC group should configure tax handling by country, entity, and transaction type. Don’t let one VAT code structure flow across all companies just because the chart of accounts is shared.

A practical configuration approach looks like this:

- Country-specific tax codes: Saudi and UAE transactions should not sit under one broad tax bucket.

- Entity-level approval rules: Each company should follow its own compliance workflow.

- Document-based treatment: Import service invoices, exports, domestic sales, and inter-company charges need separate logic.

- Reporting by jurisdiction: Finance should see liabilities and recoveries per country without spreadsheet stitching.

Exports and evidence matter

For businesses that export goods or services from KSA, the tax treatment may differ from domestic supplies. The main operational issue is documentation. If the team can’t prove why a transaction received its treatment, the ERP record may be technically posted but still weak in an audit.

That’s why mature businesses attach shipping evidence, contract references, service descriptions, and customer status to the transaction record itself. Don’t store those details in email chains and expect tax certainty later.

Industry-Specific Implications and Common Penalties

VAT risk doesn’t look the same in every industry. The legal framework may be broad, but the operational mistakes are highly specific to how the business earns revenue.

Real estate businesses need tighter transaction classification

A real estate company can’t afford vague tax treatment across leases, service charges, deposits, and sales-related documents. The finance risk usually appears when commercial and residential activity is handled through similar billing workflows.

A practical failure looks like this: the leasing team raises customer documents from a general template, accounting adjusts the tax coding later, and contract-level visibility disappears. That creates reconciliation problems and makes audit support harder than it should be.

Manufacturing businesses must connect purchases to recovery logic

Manufacturers often deal with imported raw materials, machinery, spares, production overhead, and project-style capital expenditure. VAT handling breaks down when procurement, stores, and finance operate in separate systems.

A disciplined manufacturer should focus on:

- Purchase coding accuracy: Raw materials, services, and capital items shouldn’t all be treated the same way.

- Fixed asset linkage: Machinery purchases need proper asset registration and tax support.

- Production traceability: Costing and tax documentation should connect instead of sitting in different files.

- Supplier document review: Input recovery depends on the quality of what AP receives and posts.

Trading and retail businesses face invoice-volume risk

For distributors and retailers, the threat is usually volume rather than complexity per transaction. A small tax setup error repeated across many invoices creates a large reconciliation problem. Multi-branch operators are especially exposed if one branch uses different billing habits from another.

This gets even more important at the point of sale. Retail-facing companies that want more control over tax handling, receipt structure, and branch consistency should review how a proper point of sale system works within the wider accounting environment.

The common penalties are usually self-inflicted

The verified data already confirms one direct penalty: failure to register can result in 10,000 SAR. Beyond that, businesses usually create exposure through familiar operational failures rather than obscure tax theory.

Watch for these patterns:

- Late registration: The business crossed the threshold, but nobody was monitoring taxable supplies properly.

- Wrong tax coding: Sales or purchases were posted with broad default codes.

- Non-compliant invoicing: The invoice process sat outside the core system.

- Late filing behaviour: Finance depended on manual consolidation from branches.

- Weak audit trail: Support documents were scattered across emails and folders.

Take the Next Step with Hinawi ERP

If your business is serious about vat in saudi arabia, stop treating compliance as a finance clean-up exercise. The right answer is operational control inside one integrated system.

Manual work creates delay. Disconnected software creates inconsistency. Spreadsheet-driven VAT management creates exposure. That’s the pattern across trading companies, contractors, manufacturers, schools, garages, and real estate businesses throughout the GCC. The businesses that stay organised build VAT and e-invoicing logic directly into their daily transaction flow.

What decision-makers should demand from their ERP

Your ERP should do more than post journal entries. It should support the way GCC businesses operate.

The minimum standard should include:

- VAT and e-invoicing compliance: Tax calculation, invoice structure, reporting support, and cleaner audit trails

- Real-time accounting integration: Every module should update finance without duplicate data entry

- Arabic and English bilingual operation: Branch teams and finance users need practical usability

- Flexible policy settings: Approval rules, document flow, and company-specific controls should be configurable

- Industry-specific coverage: Accounting alone isn’t enough if your business also runs projects, payroll, inventory, contracts, assets, or service operations

Why integrated regional software matters

A regional ERP makes practical sense, as Hinawi ERP’s VAT functionality is designed around Gulf business requirements. The wider platform has been developed in Abu Dhabi since 1998 to support Accounting, HR & Payroll, Real Estate Management, Fixed Assets, Manufacturing, Garage & Maintenance, School Management, CRM, and broader business automation.

For GCC companies, that matters because VAT doesn’t live alone. Payroll affects cost centres. Fixed assets affect recoveries and controls. Projects affect billing. Inventory affects valuation and purchase flow. Real estate affects contract-based invoicing. The system has to connect all of it.

A practical ERP for this market should also support:

- UAE WPS payroll support for companies running regional operations

- Factories and manufacturers needing costing and production-linked accounting

- Contracting and real estate companies needing contract and payment visibility

- Garages, schools, and service businesses needing transaction accuracy without manual duplication

The right move now is to modernise before compliance pressure forces you to. Reduce manual work. Improve financial accuracy. Give management better control over operations and reporting.

Talk to the Hinawi ERP team if you want a practical review of your current setup, your KSA VAT workflow, or your multi-country GCC process design.

Explorer Computer LLC – Hinawi Software ERP supports companies across the UAE and GCC with integrated business software built for regional realities. If you want to modernise accounting, HR & Payroll, real estate operations, fixed assets, manufacturing, garages, schools, CRM, and VAT compliance in one system, visit Explorer Computer LLC – Hinawi Software ERP or request a personalised demo through the consultation options above.