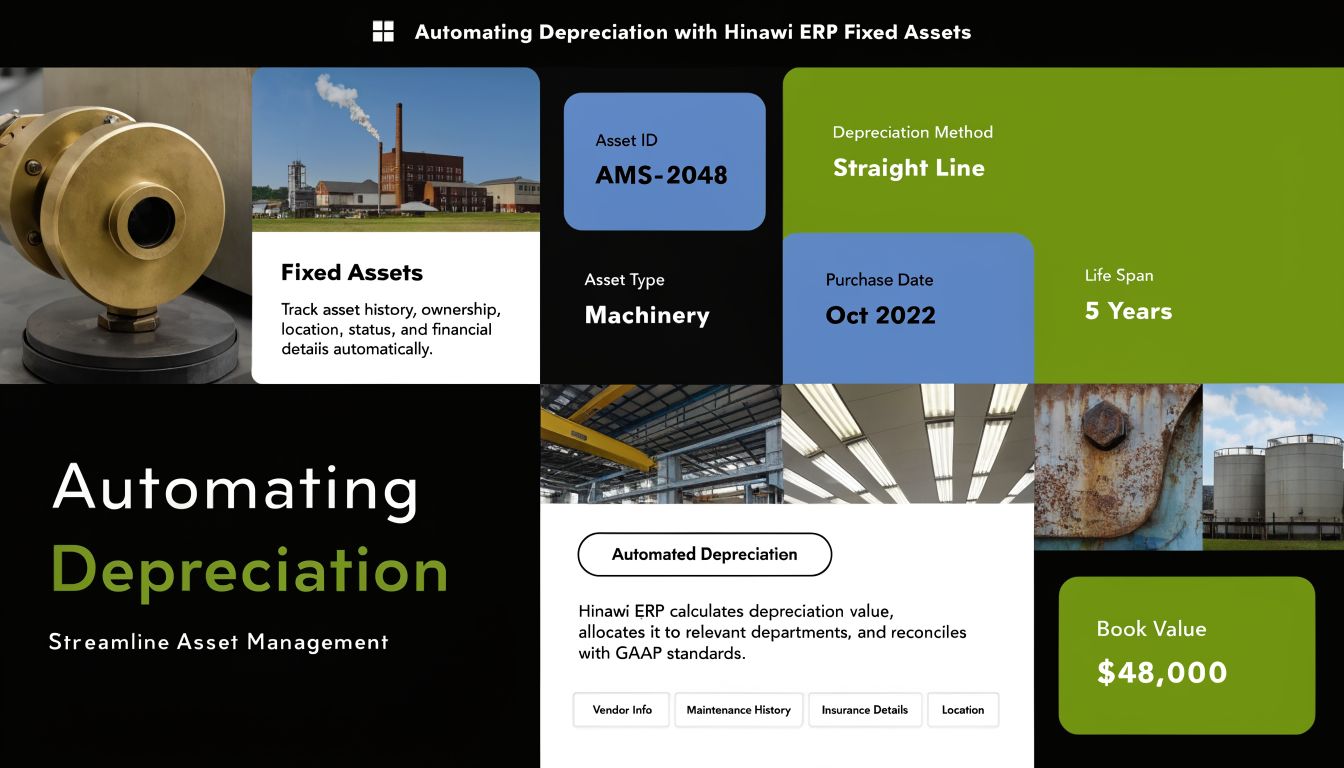

Category: Fixed Assets

A Sharjah manufacturer buys a CNC machine on 18 September. The supplier invoice is posted, the bank payment clears, and operations start using the asset immediately. Then the core accounting question hits. What depreciation method will you apply, from which date, how will you handle the partial year, and will your fixed asset schedule agree with your general ledger at month-end?

Straight line depreciation answers that question cleanly, but only if you set it up properly. Get the asset cost wrong, ignore residual value, miss the in-service date, or leave calculations in spreadsheets, and the mistakes flow straight into profit, tax, and audit support. UAE companies cannot afford that now. Depreciation affects accounting profit, deferred decisions on disposals, and the records you need to support Corporate Tax positions for financial years beginning on or after 1 June 2023.

For many UAE and GCC businesses, straight line is the right default because it is easy to govern and easy to audit. That does not mean you should treat it casually. You need a controlled fixed asset register, consistent useful life policies, and monthly posting discipline tied to the general ledger in accounting. If your team still calculates depreciation manually at month-end, fix that process before it creates reporting errors you will spend the quarter cleaning up.

Hinawi ERP helps close the gap between policy and execution. You can define asset classes, start depreciation from the correct service date, handle partial-year charges, and keep book values and journal entries aligned without relying on disconnected files. That is how fixed assets should be managed. Consistently, traceably, and with tax and audit consequences in mind.

Understanding Straight Line Depreciation in a Business Context

A Dubai contracting company buys new equipment for projects across multiple sites. The asset will be used for years, but the full cost shouldn't hit one month's profit and loss statement. That would distort performance. Accounting spreads the cost over the period the asset is expected to benefit the business. That spread is depreciation.

Straight line depreciation is the most direct version of that logic. It allocates the depreciable amount evenly over the asset's useful life. It's commonly used because management wants a stable expense pattern, accountants want consistency, and auditors want a schedule they can trace without guesswork.

According to CFI's explanation of straight-line depreciation, the annual expense is calculated as (asset cost − salvage value) ÷ useful life, so the same amount is recognised each year until the asset reaches residual value. That even-spread approach is especially useful for budgeting, branch reporting, and audit trails.

Why business owners should care

This isn't just for accountants.

If depreciation is wrong, several things go wrong at once:

- Profit reporting becomes unreliable. Monthly management accounts stop reflecting real operating cost.

- Asset values stay inflated. That creates a weak balance sheet and bad disposal decisions.

- Tax calculations become harder to defend. A poor fixed asset register creates unnecessary exposure during review.

- Budgeting suffers. Stable cost allocation matters when you're planning by branch, department, or project.

Practical rule: If an item will serve the business over multiple periods, finance should decide immediately whether to capitalise it, expense it, and if capitalised, how to depreciate it.

Where ERP makes the difference

The biggest problem isn't the formula. It's discipline. Businesses often buy assets through procurement, record them in accounting, track them in Excel, and forget to update transfers, disposals, or revised useful lives. That's exactly how fixed asset registers drift away from reality.

A proper ERP setup links the fixed asset register, depreciation schedule, and general ledger. If you want a stronger accounting base overall, it helps to align depreciation control with your broader ledger structure in accounting.

The Core Formula and Its Components

Straight line depreciation only works well when the inputs are correct. The formula is simple. The hard part is deciding what belongs in each input and documenting it consistently.

The basic formula is:

(Asset cost − salvage value) ÷ useful life

The Hartford notes that under straight-line depreciation, the annual charge comes from subtracting salvage value from cost basis and dividing by useful life, producing a constant expense. It also stresses that the cost basis must include capitalised acquisition costs such as freight, installation, and applicable taxes, otherwise depreciation is understated and carrying value stays too high (The Hartford on straight-line depreciation and cost basis).

Asset cost is more than the invoice

Many UAE companies make mistakes by booking only the supplier invoice as the asset value and ignoring directly attributable costs.

In practice, asset cost may include:

- Purchase price. The base amount paid to the supplier.

- Freight and delivery. If the cost was necessary to bring the asset to site, it usually belongs in the asset cost.

- Installation charges. If technicians had to install and commission the asset, that cost may need to be capitalised.

- Applicable taxes and related acquisition costs. Where accounting treatment requires inclusion, they form part of the depreciable base.

If you exclude these items, your annual depreciation charge will be too low. That sounds harmless until you realise your balance sheet is overstated for years.

Salvage value needs judgement

Salvage value is the expected residual value at the end of the useful life. In plain terms, it's what you think the asset will still be worth when you stop using it.

This estimate shouldn't be lazy. If your business regularly sells used vehicles, workshop machines, laptops, or generators, finance should use that experience. If your assets usually have no meaningful resale value by the end of use, the salvage value may be minimal.

Don't set salvage value mechanically just to reduce depreciation. That only pushes today's expense into tomorrow's problem.

Useful life must reflect business reality

Useful life is the period over which the asset is expected to provide economic benefit. It is not just a technical specification from the supplier brochure. A machine may physically last longer than the period your business intends to use it.

Review useful life based on real conditions such as:

- How long operations expect to use the asset.

- Whether technology replacement is frequent.

- Whether project handovers or contract cycles shorten actual usage.

- Whether maintenance policy extends or shortens service life.

A branch-heavy UAE business should define useful lives by asset class and apply them consistently. That gives finance, auditors, and management one clear policy instead of case-by-case improvisation.

Chat on WhatsApp +971506228024 Quotation – Demo Request

Step-by-Step Calculation with Worked Examples

A UAE business buys equipment on 17 April, puts it into use on 25 April, and closes monthly accounts across three branches. Straight line depreciation looks easy until finance has to calculate the first month correctly, keep branch treatment consistent, and defend the numbers during audit or Corporate Tax review. That is where fixed asset discipline pays off.

Start with the full-year calculation. Then apply your policy for partial periods. Do not improvise branch by branch.

Example one full-year depreciation

Use a simple case first.

- Asset cost: AED 100,000

- Residual value: AED 20,000

- Useful life: 5 years

Depreciable amount = AED 100,000 − AED 20,000 = AED 80,000

Annual depreciation = AED 80,000 ÷ 5 = AED 16,000

If the asset is in service for a full financial year, the charge stays the same each year.

| Year | Annual depreciation | End-of-year book value |

|---|---|---|

| 1 | AED 16,000 | AED 84,000 |

| 2 | AED 16,000 | AED 68,000 |

| 3 | AED 16,000 | AED 52,000 |

| 4 | AED 16,000 | AED 36,000 |

| 5 | AED 16,000 | AED 20,000 |

This method works well for office fit-outs, furniture, servers, leasehold improvements, and equipment that delivers value evenly over time. It also makes budgeting easier because management knows the expense pattern in advance.

Example two partial-year depreciation

It is here that many UAE finance teams make avoidable errors.

Assume the same asset is ready for use on 1 April, and the company applies monthly proration. Annual depreciation is still AED 16,000. Monthly depreciation is AED 1,333.33.

If the year ends on 31 December, the business records depreciation for 9 months in year one:

AED 16,000 × 9/12 = AED 12,000

| Period | Calculation | Depreciation |

|---|---|---|

| Year 1 (Apr to Dec) | AED 16,000 × 9/12 | AED 12,000 |

| Year 2 | Full year | AED 16,000 |

| Year 3 | Full year | AED 16,000 |

| Year 4 | Full year | AED 16,000 |

| Year 5 | Full year | AED 16,000 |

| Final period | Balance to residual value | AED 4,000 |

The rule is simple. Depreciation starts when the asset is ready for use, not when the supplier invoice is dated and not when the payment is made.

That date matters for Corporate Tax as well. If your accounting records show inconsistent in-service dates, your depreciation expense may still be valid under accounting standards, but your tax adjustments and supporting schedules become messy. Fix the policy early. Apply it the same way across all entities, branches, and asset classes.

A practical policy for UAE and GCC companies is monthly proration by in-service date. It is easier to control, easier to audit, and easier to automate in ERP.

Example three grouped asset purchases

Now take a common GCC rollout scenario. A new branch opens in Dubai or Riyadh and receives 20 laptops, 10 barcode scanners, and 15 office chairs in one month. The calculation logic does not change. The control risk does.

If a company buys 10 laptops at AED 5,000 each, with no residual value and a useful life of 3 years, the numbers are:

- Total cost: AED 50,000

- Depreciable amount: AED 50,000

- Annual depreciation: AED 50,000 ÷ 3 = AED 16,666.67

You can calculate this as one grouped asset if your policy allows it, but that is only sensible when the assets have the same purchase date, same useful life, same location, and low disposal risk. For laptops, handheld devices, and mobile equipment, that shortcut usually causes trouble later.

Track these items at unit level or at least by controlled batch:

- Asset tag or serial number

- Branch and department

- Custodian or employee assignment

- In-service date

- Transfer history

- Disposal or loss date

A spreadsheet can calculate depreciation. It cannot control movement, custody, and disposals reliably across multiple branches.

Recommended approach for UAE businesses

Use a fixed asset policy that finance can enforce, operations can follow, and auditors can test.

- Set standard useful lives by asset class

- Use residual values only when they are supportable

- Start depreciation from the ready-for-use date

- Apply one proration rule across the business

- Review additions, transfers, and disposals every month

- Match the fixed asset register to the general ledger monthly

If your team still struggles with posting flow after calculating the schedule, review these UAE journal entry examples for fixed asset accounting and align the depreciation register with the chart of accounts from day one.

Hinawi ERP helps here because the calculation does not stay trapped in a spreadsheet. You can store in-service dates, assign asset classes, calculate partial-year depreciation automatically, and keep branch-level visibility without rebuilding formulas every month. That saves time, but of greater value, it cuts audit issues and year-end cleanup.

Chat on WhatsApp +971506228024 Quotation – Demo Request

Recording Journal Entries and Financial Reporting

Depreciation isn't complete until it's posted correctly. The fixed asset register may show the schedule, but the general ledger and financial statements only reflect reality after journal entries are recorded.

Cornell's legal and accounting explanation notes that straight-line depreciation is useful when benefit is time-based rather than usage-based, and that in ERP practice its deterministic postings simplify reconciliation between the fixed asset register, general ledger, and management reporting (Cornell on straight-line depreciation and auditability).

Initial asset acquisition entry

When the asset is purchased and capitalised, the typical entry is:

- Debit Fixed Asset

- Credit Bank or Accounts Payable

The exact account title depends on the asset class. For example, plant and machinery, office equipment, vehicles, furniture, or computer equipment.

Periodic depreciation entry

At each month-end or year-end, record depreciation as:

- Debit Depreciation Expense

- Credit Accumulated Depreciation

This is the core entry finance teams must post consistently. The expense hits the profit and loss statement. The accumulated depreciation sits against the asset on the balance sheet, reducing net book value without removing the original cost.

If your team wants a practical reference for posting structure, review these journal entries in UAE accounting practice.

The original asset cost should remain visible. Don't post depreciation by reducing the asset cost account directly unless your accounting framework specifically requires a different presentation.

Disposal entries

When an asset is sold, scrapped, or retired, the accounting needs three steps:

- Remove the original asset cost.

- Remove accumulated depreciation.

- Recognise any difference between proceeds and carrying value as gain or loss.

A disposal without proper cleanup leaves dead assets sitting in the register. That's common in businesses that focus on purchase approval but ignore end-of-life controls.

Financial statement impact

Straight line depreciation affects reporting in two places:

| Statement | Impact |

|---|---|

| Profit and loss | Depreciation expense reduces accounting profit |

| Balance sheet | Accumulated depreciation reduces carrying amount of fixed assets |

That's why depreciation is not a background process. It directly affects profitability, asset values, and management decision-making. If a branch manager sees inflated profit because assets were never depreciated properly, the reporting is misleading from the start.

Comparing Straight Line with Other Depreciation Methods

Not every asset should use straight line depreciation. That said, many businesses create unnecessary complexity by using advanced methods without a clear reason. If the asset's benefit is consumed evenly over time, straight line is usually the cleanest choice.

The historical context matters. Straight-line depreciation was the standard before accelerated tax methods were introduced in the U.S. in 1954, when tax rules began permitting methods such as declining-balance and sum-of-the-years’-digits. That change created tax incentives for faster early-year expensing, but straight-line remained important for financial accounting (EBSCO on the history of accelerated depreciation).

Comparison of Depreciation Methods

| Method | Expense Pattern | Calculation Basis | Best For |

|---|---|---|---|

| Straight line | Constant each period | Cost less salvage value, divided by useful life | Office assets, furniture, fit-out, assets with steady time-based use |

| Declining balance | Higher in earlier periods, lower later | Percentage applied to declining book value | Technology assets, equipment that loses value quickly |

| Units of production | Varies with actual use | Based on usage, output, or machine activity | Heavy machinery where wear depends on production volume |

When straight line is the right choice

Use straight line when:

- Benefit is time-based. Offices, back-office systems, furniture, and many support assets fit this pattern.

- You need stable reporting. This matters for budgeting, project costing, and branch comparison.

- Your usage data is weak. If you can't reliably measure output or machine-hours, usage-based methods create more noise than insight.

When another method may fit better

There are cases where straight line can be too simplistic.

For example:

- Tech-heavy environments may replace equipment early because of obsolescence.

- Production assets may wear out according to output, not calendar time.

- Vehicles or field equipment may lose value faster in earlier years.

That doesn't mean straight line is wrong by default. It means finance should match the method to economic reality, not habit.

A business should not choose a depreciation method just because the ERP allows it. Choose it because it reflects how the asset actually delivers value.

The real issue in the UAE context

The practical issue for UAE businesses isn't only method selection. It's whether accounting depreciation and tax treatment differ and whether the ERP can keep those records cleanly separated. If book and tax logic diverge, your team needs method controls, date controls, and clear policy ownership. Otherwise year-end adjustments become messy and hard to defend.

Tax and Regulatory Rules for UAE and GCC Companies

Your finance team closes the month. The P&L includes depreciation. Then tax season arrives, and nobody can clearly explain which assets were capitalised, when depreciation started, or whether book treatment matches the tax file. That is a control failure, not a calculation issue.

For UAE and GCC companies, straight line depreciation needs to be managed as both an accounting policy and a tax support process. The UAE Corporate Tax regime made that unavoidable for businesses within scope from the applicable financial periods. If your fixed asset records are weak, tax adjustments, audit questions, and year-end cleanup will follow.

What your policy must cover

Write the policy down and apply it consistently across all entities, branches, and departments. At minimum, it should define:

- Capitalisation threshold. Set a clear rule for what goes to fixed assets and what stays in operating expense.

- Asset classes. Separate IT equipment, vehicles, machinery, furniture, leasehold improvements, and other categories.

- Depreciation method by class. Assign the method centrally. Do not leave this to user choice.

- Useful lives. Set standard lives by class and require approval for exceptions.

- Partial-year treatment. Decide whether depreciation starts by day, month, or a fixed cut-off rule.

- Residual value treatment. State when residual values are used and who approves them.

- Disposals and write-offs. Define approval, timing, and documentation requirements.

Partial-year treatment deserves special attention in the UAE. Businesses often buy assets mid-month, place them in service later than the invoice date, or transfer assets between branches. If your policy does not clearly state whether depreciation starts from the purchase date, in-service date, or the next month, your schedules will become inconsistent fast.

Tax treatment needs discipline

Do not assume book depreciation and tax treatment will always match.

In practice, UAE businesses often need a clean trail from invoice to capitalisation to depreciation start date to disposal. That matters when reviewing deductible expenses, supporting tax computations, and explaining differences between management accounts and tax working papers. The same issue appears across the GCC, especially in groups operating in more than one jurisdiction with different filing expectations and internal approval rules.

A simple rule works best. Maintain one controlled fixed asset register, and if tax treatment differs from book treatment, track that difference separately instead of burying it in manual year-end adjustments.

What auditors and tax reviewers will look for

They will expect evidence that your fixed asset process is controlled, repeatable, and tied to the ledger.

That means:

- The fixed asset register agrees to the general ledger.

- Each asset has a documented acquisition date and in-service date.

- Depreciation starts according to policy, not user preference.

- Transfers, reclassifications, and disposals are logged and approved.

- Useful life or residual value changes are authorised and traceable.

- Book and tax adjustments can be identified without rebuilding the register in Excel.

If you want a practical overview of the compliance environment behind these controls, review Hinawi's summary of the new UAE Corporate Tax rules and business impact.

Practical recommendation for UAE and GCC SMEs

Keep the method simple. Keep the records strict.

For most SMEs, straight line is the right default for standard asset classes because it is easy to apply, easy to review, and easy to automate. The common mistakes are not technical. They are operational. Wrong in-service dates, inconsistent partial-year calculations, undocumented disposals, and spreadsheet overrides cause more trouble than the formula itself.

Set the policy once. Enforce it in the ERP. Review exceptions monthly, not at year-end.

Automating Depreciation with Hinawi ERP Fixed Assets

Manual depreciation control breaks down fast. One spreadsheet handles a few assets. Then the business grows. New branches open. Project teams buy equipment directly. IT replaces devices early. Workshop assets move between sites. At that point, finance doesn't have a depreciation problem. It has a control problem.

The practical fix is automation inside a fixed asset module tied to accounting. Hinawi ERP is one example used in the region for this purpose, with fixed asset functionality designed to calculate monthly straight line depreciation and integrate postings into accounting workflows. You can review the system's fixed assets module information.

What automation should do

A proper fixed asset setup should let finance:

- Define asset classes once with default useful life, depreciation method, and accounts.

- Register assets centrally with cost, in-service date, branch, custodian, and serial details.

- Generate periodic depreciation automatically without rebuilding schedules manually.

- Post to the general ledger in real time so the register and accounts stay aligned.

- Track disposals and transfers with a clear audit trail.

What this changes operationally

When fixed assets are managed inside ERP, several recurring problems disappear:

| Manual problem | Automated outcome |

|---|---|

| Different files by branch | One central register |

| Missed monthly postings | Scheduled depreciation runs |

| Unclear asset location | Custody and branch visibility |

| Disposal not reflected in accounts | Controlled de-recognition workflow |

Chat on WhatsApp +971506228024 Quotation – Demo Request

The strongest benefit isn't speed alone. It's control. Finance can stop chasing missing details at month-end and start reviewing exceptions instead. That's where an ERP should help.

Take the Next Step with Hinawi ERP

A common UAE month-end problem looks like this. One asset was bought mid-month, another moved to a different branch, a third was disposed of, and finance is still trying to calculate straight line depreciation from spreadsheets while checking whether the postings, useful lives, and in-service dates match company policy. That is how reporting errors start, and it is exactly why fixed assets should sit inside the ERP, not outside it.

Hinawi ERP gives UAE and GCC companies a practical way to control the full asset cycle inside one system. You can set depreciation rules by asset class, handle partial-year depreciation correctly, post directly to accounting, and keep a clear record of acquisitions, transfers, and disposals. That matters for businesses that need consistent monthly closings, cleaner audit support, and better control over Corporate Tax adjustments where accounting depreciation and tax treatment do not fully match.

Hinawi ERP has been developed in Abu Dhabi since 1998 and includes Accounting, HR and Payroll, Real Estate Management, Fixed Assets, Manufacturing, Garage and Maintenance, School Management, CRM, and wider business automation. It supports VAT and e-Invoicing compliance, UAE WPS payroll, Arabic and English bilingual use, company-level policy settings, and real-time accounting integration across modules. For groups operating across branches or entities in the GCC, that structure reduces manual correction work and keeps asset data aligned with the general ledger.

If your business is still posting depreciation manually, fix that now. Use a live system that calculates on schedule, applies your policy consistently, and gives finance a reliable register for audit, tax review, and management reporting. You can review the platform at www.hinawierp.com and request a Hinawi ERP demo for your fixed asset workflow.

Chat on WhatsApp +971506228024 Quotation – Demo Request

Straight line depreciation is simple on paper. In practice, control depends on policy, timing, and system discipline. Set capitalization thresholds, define useful lives by asset category, record service start dates accurately, and automate the monthly run before asset volume becomes difficult to manage.

Take the Next Step with Hinawi ERP

For companies in the UAE and GCC, Hinawi ERP offers a fully integrated business platform developed since 1998 in Abu Dhabi. It connects Accounting, HR & Payroll, Real Estate Management, Fixed Assets, Manufacturing, Garage & Maintenance, School Management, CRM, and complete business automation in one system. The platform supports VAT and e-Invoicing compliance, UAE WPS payroll, Arabic and English bilingual use, flexible company policy settings, and real-time accounting integration across all modules.

This matters if your business wants stronger control over fixed assets, cleaner monthly closing, reduced manual work, and more accurate reporting across departments and branches. Hinawi ERP is suitable for factories, contracting companies, real estate businesses, schools, garages, trading companies, and manufacturers that need practical automation, not disconnected software.

Visit www.hinawierp.com or request a personalised demo to see how the system can help you modernise operations and improve financial accuracy.

Speak with Explorer Computer LLC – Hinawi Software ERP if your business in the UAE or GCC needs help organising fixed assets, automating straight line depreciation, improving VAT and e-Invoicing compliance, streamlining UAE WPS payroll, or connecting accounting with HR, real estate, manufacturing, garage, school, and CRM operations in one bilingual Arabic and English ERP environment.