Month-end can look clean right up to the moment the bank balance fails to match the cash book, salaries have already been released through WPS, and the VAT return is waiting for final review. At that point, the bank reconciliation statement format stops being a basic finance task. It becomes a control document that supports tax evidence, payroll traceability, and management sign-off.

That point matters in GCC finance teams because a reconciliation is rarely just about timing differences. A payment run may include salary transfers, supplier settlements, bank fees, merchant collections, and tax-related entries posted across different dates. If the format is weak, the finance manager spends more time proving what happened than resolving the difference.

Generic templates usually fall short for this reason. They capture deposits in transit and outstanding cheques, but they often ignore GCC-specific checks such as VAT treatment on bank charges, settlement tracing for WPS files, and reviewer accountability across legal entities and branches. A stronger format gives each reconciling item a clear audit trail from bank line to general ledger, which matters even more in businesses running multiple accounts, currencies, and approval layers.

That is also why the underlying ledger structure matters before the reconciliation starts. If the cash book is poorly mapped, the statement becomes a manual cleanup exercise every month. Finance teams using a well-organized general ledger structure in accounting usually close faster because each bank movement already sits against the right account, tax code, and reference.

I have seen the same trade-off across UAE and wider GCC operations. Spreadsheets can work for a small entity with low transaction volume and one reviewer. They become risky once payroll, VAT, inter-branch transfers, and audit follow-up all depend on the same file. Hinawi ERP solves that old problem in a practical way by keeping banking, accounting, payroll, and operational records in one system, so the reconciliation format is backed by source data instead of manual comments.

For a GCC finance manager, that is the standard to aim for. The statement should reconcile balances, show why differences exist, and stand up to review from auditors, tax teams, and management without a separate explanation pack.

Chat on WhatsApp +971506228024 Quotation – Demo RequestThe Anatomy of a Bank Reconciliation Statement Format

At month-end, the pressure usually shows up in the same place. The bank statement closes, payroll has already run through WPS, VAT-sensitive bank charges sit on the statement, and management wants a cash position that ties without follow-up questions. A bank reconciliation statement format has to hold up under that pressure.

A proper bank reconciliation statement format is a controlled working paper that shows how the bank balance and the ledger balance were reconciled to the same adjusted amount. For GCC businesses, that format should do more than match figures. It should also make review easier where payroll transfers, VAT treatment, and inter-account movements need to be evidenced clearly.

The most reliable layout for this is a two-column structure. One column starts from the bank statement balance. The other starts from the company’s general ledger cash balance. Each column carries only the adjustments that belong to that side until both adjusted balances agree.

What the header must contain

The header is part of the control. If it is weak, the whole statement becomes harder to review, harder to approve, and harder to support during audit, VAT review, or internal control testing.

A workable header should include:

- Entity name, using the legal company name

- Period covered, such as January 2026 or 01/01 to 31/01

- Bank account details, including bank name and masked account number

- Currency, especially where AED, SAR, USD, or other currencies are used across operations

- Prepared by and reviewed by fields, with approval dates where your policy requires them

For GCC finance teams, I also recommend one more point in the header or reference block. Identify whether the account is used for supplier payments, customer collections, WPS payroll, VAT settlements, or mixed transactions. That single detail saves time during review because a payroll account should be assessed differently from an operational collections account.

Practical rule: If a reviewer cannot identify the legal entity, account, period, and purpose of the bank account within a few seconds, the format is too weak.

Support behind each reconciling item matters as much as the table itself. Each item should show the date, amount, description, reference, and supporting document, then carry preparer and reviewer sign-off under your internal control policy. For a WPS-related transaction, that support may include the payroll file reference or bank transfer confirmation. For a bank charge, it may include the statement line and the tax treatment recorded in the books.

The standard table layout

Below is the structure I recommend for most UAE and GCC finance teams.

Standard Bank Reconciliation Statement Format (as of 31-XX-2026)

| Particulars | Amount (AED) | Particulars | Amount (AED) |

|---|---|---|---|

| Balance as per bank statement | Balance as per cash book | ||

| Add deposits in transit | Add interest income or direct credits not yet recorded | ||

| Less outstanding cheques | Less bank fees and charges not yet recorded | ||

| Less or add bank-side corrections if applicable | Less direct debits or book errors if applicable | ||

| Adjusted bank balance | Adjusted cash book balance |

This format works because it separates timing differences from book adjustments. That distinction is not cosmetic. It affects review quality, ageing of open items, and how quickly the team can identify whether the issue sits with bank timing, posting discipline, or a genuine error.

For GCC businesses, the standard format often needs two practical enhancements. First, add a reference or note field for VAT treatment on bank-side charges and fees where applicable. Second, clearly tag items linked to WPS payroll transfers, salary protection clearing, or payroll rejections, because those items often draw extra scrutiny from finance leadership and auditors.

What works and what fails

What works is a statement that is short, traceable, and disciplined. Every line should tie back to a bank statement entry, deposit advice, journal, payroll support, or approved correction.

What fails is a format that turns into a parking area for unresolved items. If outstanding cheques, direct debits, payroll returns, bank charges, and ledger mistakes are all mixed together, the reconciliation may still total correctly while control quality remains poor. That is how old items stay open for months and then resurface during audit or VAT review.

The format should also tie back to the ledger structure used in accounting control, not just to a spreadsheet prepared for month-end. In practice, that is where many teams see the difference between a reconciliation that only balances and one that can be reviewed, approved, and closed with confidence.

Defining Key Reconciling Items for GCC Businesses

A reconciliation usually breaks down at the classification stage, not at the addition stage. I see this often with GCC finance teams. The statement balances on paper, but review gets delayed because payroll returns, bank charges, card settlements, and stale cheques are grouped under vague labels.

Clear item definitions solve that.

Core items every team should classify correctly

Deposits in transit are receipts recorded in the books before the bank reflects them at period-end. These often come from late customer deposits, POS batch settlements, or collection files submitted near month-end.

Outstanding cheques are payments already posted in the ledger but not yet presented to the bank. In supplier-heavy businesses, some of these are genuine timing items. Others are old instruments that should be followed up, cancelled, or reissued instead of rolling forward month after month.

Bank fees and charges hit the bank statement before the accounting entry is posted. The finance team needs to book them promptly and review the VAT treatment based on the supporting bank document and the nature of the charge.

Interest income appears in the bank first and needs a matching entry in the books with the correct income code and period.

GCC-specific items that generic templates usually miss

Generic templates often fail in two areas. The first is VAT treatment on bank-related entries.

A line labelled only as "bank charges" is weak control. The description should show the charge amount, date, bank reference, whether VAT applies, and what support backs the posting. That matters in the GCC because a reconciliation is often reviewed alongside the VAT return workpapers. If the charge is posted net, gross, or to the wrong tax code, the problem usually surfaces later during return review rather than during the bank rec itself.

The second area is WPS payroll reconciliation.

A payroll run is not fully reconciled just because HR approved it and the bank accepted the upload file. The bank reconciliation has to confirm that the bulk salary transfer cleared as expected, then isolate rejected salaries, reversals, name mismatches, inactive accounts, or partial releases. In UAE entities, that review should tie back to WPS support and the payroll clearing account, not just the final debit on the bank statement.

A BRS that does not trace salary EFTs to actual bank settlement leaves a control gap between payroll approval and employee payment.

That gap creates real operational risk. Salary complaints escalate quickly, and unresolved WPS-related differences can trigger management attention well before month-end close is complete. In practice, I advise finance managers to give payroll-related reconciling items their own category in the format instead of burying them inside miscellaneous payments.

A practical classification lens

Use three tests for every open item:

- Has the bank processed it already

- Has the company recorded it already

- Does it affect VAT, WPS payroll, or another regulated reporting trail

If the bank has processed the item but the books have not, it usually needs a journal entry or correction on the company side. If the company has recorded it but the bank has not, it is usually a timing difference that needs ageing and follow-up. If the item touches payroll or VAT, the narration and support should be tighter than for an ordinary receipt or payment.

Teams get better control when this logic sits inside their accounting system and approval workflow, especially where bank posting, payroll review, and ledger control are split across different users. Hinawi ERP helps here by keeping bank transactions, tax coding, payroll clearing, and audit support connected in one record, which reduces the usual spreadsheet handoffs that create classification errors.

A Step-by-Step Guide to Preparing the Statement

Month-end in a GCC business rarely fails because the format is wrong. It fails because the reconciliation is prepared out of sequence, payroll support sits outside finance, or VAT-sensitive entries are posted after the statement is signed off.

Step 1 Gather the source records

Pull the full record set before anyone starts matching. That means the bank statement for the period, the bank or cash ledger, and the prior month’s signed reconciliation with its open-item schedule.

For GCC entities, add the records that carry compliance consequences. Include WPS salary transfer support where payroll is paid through bank files or exchange houses. Include bank advices for customer receipts where VAT timing matters, especially if collections and tax invoicing do not land on the same day. If the account receives merchant settlements, financing deductions, or direct debit collections, keep those schedules in the file from the start.

Keep unresolved prior-period items visible. A cheque or transfer that rolls month after month is no longer a routine timing item. It needs ownership, ageing, and a decision.

Step 2 Match transactions line by line

Match the bank statement to the ledger in a fixed order. Receipts first. Payments next. Bank-originated items after that.

This stage needs discipline. Teams create avoidable noise when they start explaining differences before completing the basic matching.

Use a practical review sequence:

- Clear exact matches first, including value, date, and reference where available.

- Separate timing differences such as deposits in transit, unpresented cheques, and transfers initiated near period-end.

- Identify bank-originated activity such as charges, interest, reversals, returned payments, and direct debits that may still be missing from the books.

- Isolate regulated items such as WPS salary settlements, VAT-related collections, and bank fees that require the correct tax and account treatment.

- Escalate unusual lines such as duplicated EFT references, net settlements with deductions, or receipts that cannot be tied to a customer account.

In practice, payroll lines deserve extra care. A salary file can be approved in payroll, funded in treasury, and settled by the bank on a different date. If the WPS instruction, payroll clearing account, and bank posting do not align, the reconciliation should show that clearly instead of hiding it inside a generic outstanding payment total.

Step 3 Build the draft statement

Move the unmatched items into the statement format once the matching is complete. Timing differences stay on the reconciliation. Items already processed by the bank but missing or wrong in the books must be posted to the ledger.

A clean draft does two things. It explains the difference, and it shows what action is required.

Use simple categories that support review and compliance:

- deposits in transit

- unpresented cheques or transfers

- bank charges and commission

- interest and bank credits

- direct debits and standing instructions

- WPS payroll settlement differences

- unidentified receipts or payments under investigation

If the draft still looks cluttered, the problem is usually classification. Finance teams often mix timing items with correction items, which makes the statement harder to approve and harder to clear next month.

Disconnected spreadsheets make this worse. Hinawi ERP keeps bank activity, journals, payroll clearing, and tax coding in one workflow, so the reconciliation is built from the same transaction history used for reporting and review.

Step 4 Post the required journal entries

The reconciliation is not finished until the ledger reflects items the bank has already processed. Common entries include bank fees, interest income, direct debits, returned transfers, and receipt allocations that were posted to the wrong account.

For GCC businesses, this step also affects compliance. Bank charges may need the company’s approved tax treatment in the books. Payroll-related corrections must agree with the salary clearing logic and WPS support retained by HR and finance. Where the bank statement shows merchant fees or deductions from customer collections, the narration should be clear enough for both audit review and VAT file support.

Delaying these entries creates repeat breaks in the next close cycle. If your team posts month-end adjustments from staging files, standardise that process with tools for importing journal entries from controlled templates.

Step 5 Review and sign off

Finish with a proper review pack, not just a reconciled number. The file should include the final statement, the adjusted balance tie-out, support for every open item, evidence of journal posting, and preparer and reviewer approval under the company’s authority matrix.

Reviewers should ask direct questions. Is every old item still valid. Has payroll been fully settled through the bank. Do bank-originated charges and credits have the right account and tax treatment. Are unidentified receipts parked and followed up, rather than forced into revenue to make the balance agree.

That review standard matters. A bank reconciliation is not just a month-end form. It is a control document that links cash, payroll settlement, VAT-sensitive postings, and audit evidence in one place.

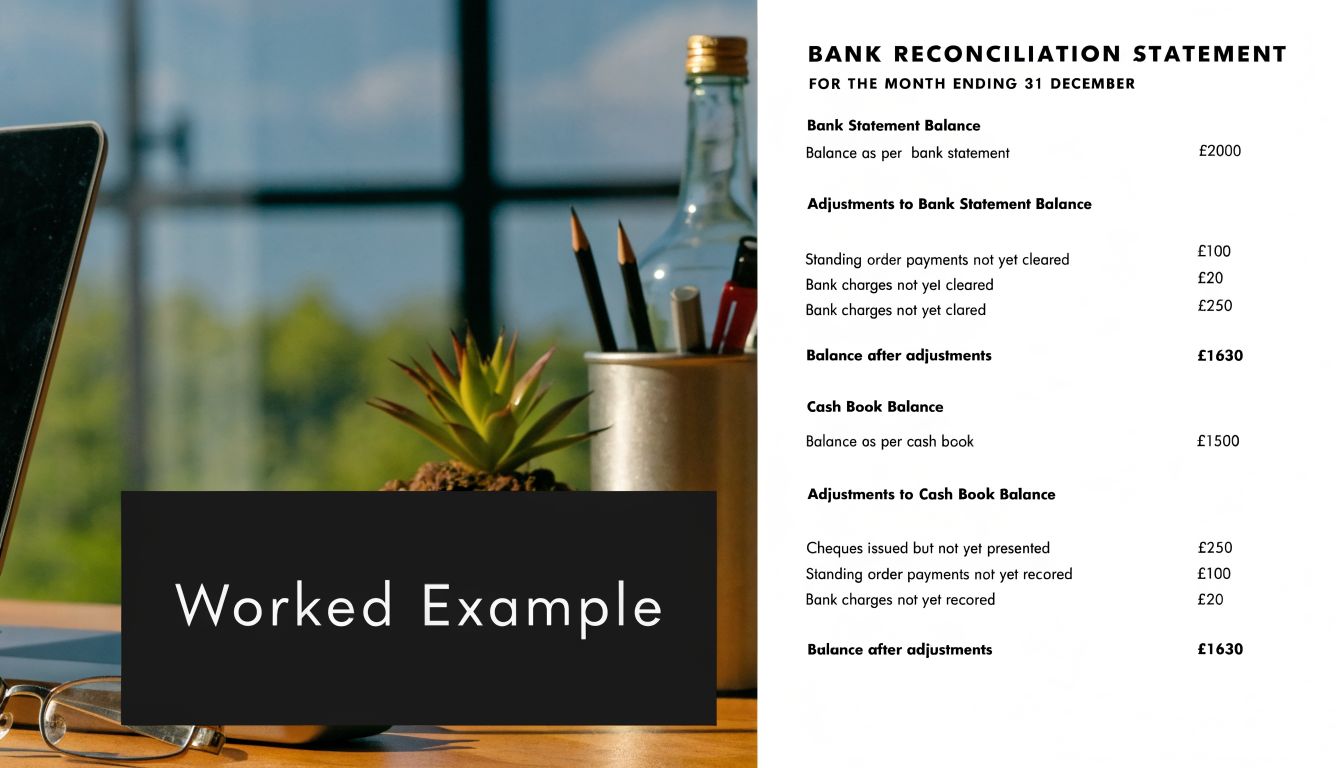

Worked Example A Standard BRS in AED

Month-end in Abu Dhabi often looks like this. The bank statement closes at AED 250,000, the general ledger shows a different figure, and the finance manager needs a reconciliation that will stand up to review, audit, and tax support. In a normal UAE trading business, the differences usually come from timing items plus a few bank-posted entries that never reached the books.

Assume the finance team identifies four items for the month:

- Customer receipt lodged late: AED 15,000

- Supplier cheques not yet presented: AED 8,500

- Bank service fee charged by the bank: AED 500

- Interest credited by the bank: AED 300

The bank side calculation

Start with balance as per bank statement: AED 250,000.

Then adjust only for timing differences already recorded in the company books:

- Add deposits in transit: AED 15,000

- Less outstanding cheques: AED 8,500

The adjusted bank balance is AED 256,500.

The book side calculation

Now correct the cash book for items the bank has processed but the company has not yet posted.

If the cash book balance before adjustment is AED 256,700, apply these entries:

- Less bank fees: AED 500

- Add interest income: AED 300

The adjusted cash book balance is AED 256,500.

Both adjusted balances now agree. That is the control point.

What a GCC finance manager should check

In practice, this simple AED example is where compliance discipline shows up. If the AED 15,000 receipt relates to a taxable sale, the VAT treatment should already be supported in the sales and receipt trail. The reconciling item does not change VAT by itself, but weak narration can create questions during file review. The same applies if bank deductions relate to merchant settlement fees or collection charges. The ledger posting should make the nature of the deduction clear.

Payroll needs the same care. If a bank debit in the statement is linked to salary transfers, the amount and date should align with the WPS funding file and the salary clearing account, not be left as an unidentified bank movement.

A finance manager should separate the items clearly:

- Timing differences stay on the reconciliation. They do not need new journal entries.

- Bank-originated items must be posted to the ledger.

- Compliance-sensitive items such as payroll settlements, merchant charges, and customer collections need narration that supports VAT and WPS review.

Journal treatment for this example

The book entries are straightforward:

- Bank charges entry: Dr Bank Charges Expense AED 500, Cr Bank AED 500

- Interest entry: Dr Bank AED 300, Cr Interest Income AED 300

Attach the bank statement line for each posting. That saves time during reviewer queries and prevents the same item from appearing again next month.

Where teams still pull bank activity from one system and post journals in another, mapping rules matter. A controlled workflow using QuickBooks integration rules for bank-linked accounting entries reduces coding errors and keeps recurring charges, interest, and receipt allocations consistent.

The value of this format is not the arithmetic. It is the audit trail. A clean AED reconciliation shows which items are timing-related, which require accounting entries, and which need compliance support before close is signed off.

Advanced Scenarios Multi-Currency and Multi-Branch Reconciliation

A single AED current account is the easy case. Complexity appears when the business operates with foreign currency accounts, branch-level cash movements, or both.

Multi-currency accounts

If the company holds a USD account alongside AED operations, the reconciliation has two layers. The accountant must match the foreign currency transactions to the bank statement, then ensure the accounting treatment in the base reporting currency remains correct under the company’s accounting policy.

In practice, what causes trouble isn’t the format. It’s the operational discipline. Teams often mix exchange-related adjustments with ordinary timing differences, which makes review difficult. The cleaner approach is to reconcile the bank account activity first, then address any accounting treatment required by the company’s foreign currency process.

A useful control point is to keep these items separate:

- Bank-side timing items such as pending foreign transfers

- Book-side omissions such as bank charges or direct credits

- Currency-related accounting reviews handled under the finance policy, not disguised as ordinary reconciling items

Multi-branch operations

A multi-branch company across Abu Dhabi, Dubai, or wider GCC markets shouldn’t rely on one person maintaining a single combined spreadsheet for all accounts. That usually creates weak accountability and inconsistent narration.

A better operating model is:

| Reconciliation level | Control practice |

|---|---|

| Branch account | Reconcile by legal entity, account, and branch responsibility |

| Shared treasury account | Keep a separate reconciliation with branch references where needed |

| Head office review | Consolidate only after branch-level reconciliations are complete |

Branch-level reconciliation should answer one question first. Is the bank account for that branch clean on its own before anyone talks about consolidation?

Integrated systems make this easier because rules, account mappings, and approval logic can be standardised across locations. Where businesses also rely on external or complementary tools, they should define clear integration rules for accounting workflows so duplicated or mismapped bank entries don’t create false reconciling differences.

Common Errors and Troubleshooting Your Reconciliation

Month-end in a GCC business often breaks down in the same place. The ledger is close to balance, but one payroll reversal, one unposted bank charge, or one VAT-related receipt mapped to the wrong account leaves the reconciliation unresolved. At that point, the problem is rarely the format of the statement. It is usually weak ownership of exceptions.

Start by identifying what kind of difference you have. A clean repeated variance usually points to an entry problem. An irregular variance tied to payroll files, collections, or tax-linked receipts usually points to a process failure.

When the difference looks mathematical

Mathematical differences are normally faster to clear, but they still need a controlled review. Common causes include:

- Transposition errors, such as posting 96 instead of 69

- Transcription errors, where the amount is copied incorrectly from the bank advice or payment schedule

- Decimal and format issues, especially when imported files use inconsistent separators or currency formatting

- VAT coding mistakes, where the cash amount is correct but the entry is split incorrectly between base amount and tax

Review the largest unmatched items first. Then check entries posted on the last two or three working days of the month, because rushed cut-off entries often create small but recurring differences.

When the issue is process, not posting

In GCC finance teams, the harder reconciliation problems usually come from incomplete workflows across accounting, payroll, treasury, and operations.

Typical examples are:

- Bank charges, direct debits, or interest not recorded in the books

- Transactions posted in the wrong period

- Outstanding cheques or transfers carried forward for months without follow-up

- Duplicate entries caused by both file import and manual posting

- WPS salary transfers rejected or reversed by the bank after payroll was marked as paid

- Customer or supplier receipts affecting VAT accounts without proper ledger review

WPS exceptions need particular attention. If the bank rejects part of a salary file, the cash position, payroll liability, and employee-level payroll record can all fall out of sync. Treat that as a reconciliation exception with HR input, not as a side note outside finance.

VAT-linked cash movements also deserve a separate check. A receipt can match the bank and still be wrong in the books if output VAT, advance receipt treatment, or adjustment posting was handled incorrectly. The bank reconciliation will not fix the tax entry by itself, but it should expose the mismatch early enough for the finance team to correct it before return preparation.

A practical troubleshooting sequence

Use a consistent order. It saves time and prevents random adjustments.

- Confirm the opening balance against the last approved reconciliation.

- Check period-end unmatched lines for cut-off errors and delayed bank processing.

- Review duplicate amounts and similar narrations across imports, EFT batches, and manual journals.

- Inspect old outstanding items and assign each one to a named owner for resolution.

- Trace payroll reversals or partial salary rejections back to the WPS file, employee listing, and bank debit.

- Review unusual receipts and payments affecting VAT-related accounts so the cash match does not hide a tax posting error.

Small differences still matter.

In practice, minor unresolved items often point to a broken approval step, a weak import rule, or poor coordination between finance and HR.

What not to do

Do not insert a suspense figure inside the reconciliation just to force agreement. If your policy allows a temporary suspense account in the books, it should be approved, documented, and cleared on a defined timeline.

Do not carry stale reconciling items month after month because they look immaterial. Once an item ages without explanation, it stops being a timing difference and becomes a control issue.

Do not leave salary exceptions only with HR. If the bank rejects or reverses a payroll transfer, finance must reflect that in the reconciliation trail, because the bank movement and the payroll obligation no longer agree.

Finance teams that want tighter control usually get better results from a single system that connects bank activity, payroll, VAT, and ledger posting logic. A web-based ERP for accounting, payroll, and business management helps reduce duplicate posting, keeps exception handling visible, and gives month-end reviewers a clearer audit trail.

Chat on WhatsApp +971506228024 Quotation – Demo RequestAutomating Bank Reconciliation with Hinawi ERP

Month-end often looks the same. The bank file is in, payroll has already gone through WPS, VAT-related receipts and payments are sitting in the ledger, and the finance team is still chasing unmatched lines across separate spreadsheets. At that point, reconciliation is no longer a basic matching task. It is a control process that needs speed, traceability, and clear ownership.

What automation changes in practice

An ERP-based process shifts effort away from data entry and toward review. Bank statement activity is imported, matching rules are applied, and the finance team focuses on exceptions that need accounting judgement.

For GCC businesses, those exceptions usually follow a pattern. They are often tied to VAT settlements, WPS salary transfers, bank fees, returned payments, bulk customer collections, or inter-branch postings that do not carry clean references into the ledger. Generic matching rules help, but they are not enough if the reconciliation format has to support audit review and local compliance at the same time.

Hinawi ERP handles that better because the reconciliation sits inside the accounting record, not beside it in a separate file. A finance manager using a web-based ERP platform for accounting, payroll, and business management can review unmatched items against journal entries, payroll output, branch activity, and source documents in one place.

What works better than spreadsheets

Spreadsheets still have a place for ad hoc review. They are weak as a recurring control tool.

A spreadsheet can show that totals agree. It does not reliably preserve who prepared the reconciliation, who reviewed it, which bank line was matched to which ledger entry, and why an old exception remained open for another month. That gap matters more in GCC businesses where payroll rejections, VAT payment timing, and multi-entity cash movement can all affect the same bank account.

An integrated ERP keeps the reconciliation trail attached to the transaction history. That improves follow-up on stale items, supports reviewer sign-off, and makes it easier to explain exceptions during internal audit or external audit queries.

The trade-off finance managers should recognise

Automation improves consistency, but it does not replace finance judgement.

The system can match routine receipts and payments quickly. Finance still needs to investigate unusual charges, partial settlements, payroll reversals, duplicate postings, and items cleared by the bank but posted to the wrong branch or cost center. I usually advise finance managers to judge the system by the quality of exception handling, not by how many lines it clears automatically.

That is where Hinawi ERP adds practical value for GCC teams. It shortens the mechanical part of reconciliation while keeping VAT, WPS payroll, and ledger adjustments visible in the same control flow.

Good automation reduces clerical work and strengthens audit visibility. The accountant still decides how exceptions are resolved.

Frequently Asked Questions on BRS Compliance

How often should a company prepare a bank reconciliation statement

A finance manager in the GCC usually sees the same pressure points every month. Supplier runs cluster near month-end, WPS files go out on fixed payroll dates, and VAT payment timing can create bank movements that need explanation. In that setting, monthly reconciliation is the minimum standard.

High-volume accounts often need weekly or even daily review. I usually recommend increasing frequency for accounts used for payroll, online collections, POS settlements, or inter-branch transfers, because unresolved differences in those accounts age quickly and become harder to trace.

What should an external auditor expect to see

An external auditor will look for more than a matching balance. The file should show the bank statement used, the ledger balance on the same date, a list of reconciling items, supporting documents, who prepared the reconciliation, who reviewed it, and how long each open item has remained outstanding.

For GCC businesses, auditors also pay attention to items that affect VAT filings or payroll control. A VAT payment posted to the wrong period, a salary transfer rejection, or a bank charge left unrecorded can all turn a routine reconciliation into a wider control issue.

Can a business prepare the BRS quarterly instead of monthly

Quarterly preparation is usually a weak choice unless account activity is very low. By the time finance returns to a three-month-old difference, supporting detail may be harder to obtain, staff may not remember the transaction context, and correction entries may spill into the wrong VAT or payroll review cycle.

Monthly reconciliation keeps exceptions smaller and easier to clear. It also gives management a more reliable cash position during the period, not just after it ends.

How should payroll be reflected in the reconciliation

Payroll paid through WPS or bulk EFT should be checked at detail level, even if the bank shows a single debit. Finance should confirm that the cleared amount matches the approved payroll file, then review any rejected salaries, reversals, retry payments, or manual corrections posted after the original run.

This matters in companies where HR prepares payroll and finance posts the accounting entry from a separate system. If the rejected salary returns to bank but stays uncleared in payroll suspense or staff payable, the reconciliation may balance while the books remain wrong.

What approvals should be visible on the statement

The statement should show who prepared it, the preparation date, who reviewed it, the review date, and evidence that unusual reconciling items were examined before sign-off. Dual review is a sound control for businesses with payment authority risk or branch-level cash handling.

If one user prepares the reconciliation, posts the adjustment, and clears the exception without review, the control is weak. Most auditors will challenge that setup.

Does the BRS need to reflect VAT-related bank activity separately

Yes, where timing or coding can affect compliance. VAT payments, refunds, penalties, and bank charges linked to taxable activity should be easy to identify in the reconciliation support. The statement itself does not need a separate VAT section in every case, but finance should be able to trace each VAT-related bank movement back to the ledger and filing period without delay.

That trace matters during FTA reviews. It also matters internally when treasury, tax, and accounting do not close on the same day.

Can software improve BRS compliance without weakening control

Yes, if the system keeps the audit trail clear and does not hide exceptions behind automatic matches. Hinawi ERP is useful here because it keeps bank transactions, ledger postings, payroll activity, and review records in one accounting flow. That helps finance teams clear routine items faster while keeping VAT and WPS-related exceptions visible for investigation.

The practical trade-off is simple. Automation saves time on matching. Finance still needs to review old outstanding items, wrong-period postings, duplicate receipts, payroll rejects, and branch misallocations.

If your team is reviewing reconciliation controls or replacing spreadsheet-based processes, you can contact Hinawi directly through WhatsApp or request a demo below.

Chat on WhatsApp +971506228024 Quotation – Demo RequestA well-built bank reconciliation statement format supports cash accuracy, audit follow-up, and compliance review in the same document. In GCC operations, that format should account for VAT timing, WPS payroll exceptions, multi-branch postings, and clear reviewer sign-off.